City Council poised to vote on two ideas aimed at combating foreclosures in Oakland

on October 15, 2012

The City Council is slated Tuesday to vote on two different approaches to the problem of multiple property foreclosures in Oakland. One tries to help homeowners threatened with foreclosure in the city’s hardest-hit neighborhoods, while the other would require investors who snatch up properties under foreclosure to fix them up, both inside and out.

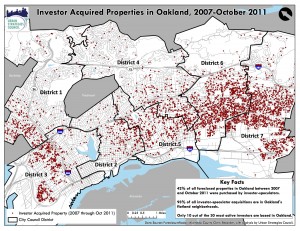

The new proposals come on the heels of a report called “Who Owns Your Neighborhood,” which was released last June and details Oakland’s foreclosure mess. The report found that big investors are buying East and West Oakland properties facing foreclosure—a trend that “destabilizes communities,” the report concluded. From 2007 to 2011, according to the report, 42 percent of the city’s 10,000 houses that banks sold after foreclosure were purchased by outside investors. Those properties “are often in poor condition due to deferred maintenance related to the age of the housing stock or recent problems associated with foreclosure and vacancy, such as squatting, vandalism and theft,” read the report, which was produced by the Oakland-based Urban Strategies Council, an advocacy group that lobbies for new policies impacting the poor.

Mayor Jean Quan introduced one of the two plans, an ambitious new city effort to help homeowners struggling to make mortgage payments on time, at a press conference last week. “Oakland has long been on the forefront—sometimes successfully, and sometimes unsuccessfully—with the issue of foreclosures and fairness around bank loans,” she told a small crowd gathered at City Hall. “We’re developing new tools that we hope will solve the greater problem… Too often, neighborhoods fall into disrepair when there are foreclosures.”

Called the “Oakland foreclosure prevention plan and mitigation initiative,” the program Quan introduced, which she said she expects will receive unanimous support from the City Council Tuesday, is a multi-tiered effort that would create a city fund aimed at preventing foreclosures before they are finalized.

Margaretta Lin, who works in the city’s Department of Housing and Community Development and is heading the initiative, said she believes it’s the most comprehensive idea being tried out in the country for combating foreclosures.

“From everything that we’re hearing from other cities, overall, what we’re creating in Oakland is unique,” Lin said. “I’ve just been asked to speak at a conference at Harvard in a few weeks to talk about what we’re doing here, so other cities can learn from us.”

At the heart of the program, which would be launched in early November if council members approve it, is a city-run bank account that would enable the city itself to purchase properties that have come under foreclosure proceedings, and then resell them back to the original homeowners at the current market rate. In the pilot year, at least $5 million would be needed, to help an estimated 20 to 25 residents. Those homeowners would be identified as the most at-risk of losing their homes, said Lin, who added that that number of residents is a reasonable amount as the city tests the program this year.

Part of that $5 million—all of which is already secured—would come from a $1.2 million grant from the U.S. Department of Housing and Urban Development, which is already approved, Lin said. Financing in the first year would also come from banks, including One Pacific Coast Bank, and other investors such as Enterprise Community Partners, an investment company based in Maryland that develops public-private partnerships to expand affordable housing programs.

“Basically what this program will do is take funds and it will buy homes that are in the threat of foreclosure, and it will sell them back to the homeowners at the current market value,” Quan said at her press conference. “A lot of people are underwater—that is, their homes are not worth as much a their original loan—and this will allow them to refinance, and we hope, save their homes.”

The plan also includes counseling, legal assistance, outreach, and referral services for families, to make them aware of recently-passed state and federal laws to help underwater homeowners.

One Oakland-based organization singled out for some of the funding for the program, Causa Justa, would receive $50,000 in the first year to train outreach workers and manage a database system for identifying homeowners in need. Another $100,000 is allocated for four other local nonprofits.

Much of the funding for these counseling and referral programs would come from violation penalties from the city’s blighted foreclosed properties program, which are already collected from offending landlords, but under the new plan money would be set aside in a special city account. Last year the city collected $1.6 million in fees and penalties from major lenders, according to Lin. Those lenders were Wells Fargo, Chase, Bank of America, Freddie Mac and Fannie Mae and U.S. Bank. Previously, money would be used for the city’s general code enforcement budget, but last summer, the City Council dedicated violations payments to foreclosure prevention programs, she added. In the first year, the city has dedicated $350,000 to these initiatives.

“We collect fines and penalties through our blighted and foreclosed properties program,” Lin said. “That pot of money would be used for foreclosure prevention activities.”

Finally, the new program includes a plan for the city to negotiate directly with banks, on behalf of some property owners in danger of foreclosure, for loan modifications. City officials would report to the public quarterly on their progress in this effort. Under state and federal laws, city staff would report to the state attorney general’s office banks that don’t approve loan modifications for eligible property owners.

“We’ll be talking to banks, and we could say ‘How come these families did not receive loan modifications, since they should have benefitted from new laws?” Lin said. “We already have commitments from Wells Fargo and Chase.”

Patricia Hanratty, who works for Community Capital, a Boston financial institution that assists low-income homeowners, said Oakland’s plan to buy properties in threat of foreclosure and then sell them back to the property owners at the current market rate, is unprecedented for a city government. She worked on a similar program in Boston, she said.

“This is the most comprehensive plan I’ve seen … and I do this work all across the country,” Hanratty said, adding that a city employee calling a bank commands more attention than an ordinary mortgage-holder.

“They actually answer the phone, which is very often not the case when a homeowner calls,” she said.

Quan called the need for such a program “urgent,” quoting from the Urban Research Council data that reported that from 2007 to 2011, more than 100,000 households in Oakland have been foreclosed upon. That’s about one in 19 households, according to the report.

Debi Mason, an Oakland resident who spoke recently at a subcommittee meeting in which council members were considering the foreclosure prevention plan, said she’s “in crisis mode.”

“We walk and we ride past these homes that are boarded up, so we see the blight,” said Mason, an Oakland resident who said she currently lives with a sister whose home is in the foreclosure process. “This is a staggering problem … there are too many people who have walked away from this great city because the battle is just too hard.”

Manuel de Paz, who also lives in Oakland and spoke at Tuesday’s press conference, said he’s currently in talks with Bank of America to obtain a loan modification for a house he’s lived in for more than a decade. He said he waited for nearly two years for a bank response regarding the modification, and recently he was told he was missing certain necessary documents.

“They never told me that they were missing from the packet I sent them, or that it was incomplete,” de Paz said.

He said he’s had to work two jobs, totaling between 12 and 14 hours a day, six days a week to pay the mortgage on a home that’s underwater.

“The question I have for the city is—how are they going to make sure this happens, for the city to buy our mortgages,” de Paz asked after the press conference. “The question is, is it too good to be true?”

The program won support from the City Council’s Community and Economic Development subcommittee following the press conference earlier this week, giving it the green light to go before the City Council Tuesday.

“It’s a very exciting program,” said Councilwoman Jane Brunner, who sits on the committee. “We’ve been doing a lot around foreclosures, but what we haven’t been able to do is get people to stay in their homes.”

If approved by the council, details for the program would be worked out at a conference on foreclosures, now set for November 11 at the downtown Oakland Marriott. There, residents could get help on foreclosure prevention efforts being undertaken by the city.

The second foreclosure-related City Council proposal, called the “non-owner occupied residential building registration,” follows the October 2 council meeting, during which a vote on the measure tied, 4-4. If adopted, the new ordinance would require investors who buy under-foreclosure properties to schedule a building inspection within 30 days, so officials can determine whether there are health and safety violations—inside the house or outside. Then the owner has 60 days to repair any violations. At present, building officials can only inspect the interior of foreclosed or blighted properties if there is a complaint or if they’re invited inside.

The new ordinance, which if approved Tuesday, would require an additional council vote at a future meeting in order to become law, would take existing city blight laws a step farther, allowing building inspectors to go inside homes to check on health and safety violations related to the building’s infrastructure, even if there’s been no formal complaint.

Initially introduced in June by Councilwoman Desley Brooks, the registration proposal would create an online database tracking investors who buy properties in Oakland. These property owners would be required to pay a $568 fee to the city for inspection and registration. However, if the new owners take out a building permit to fix up the property in the first 30 days, they’d be exempt from the registration process.

Brooks said that with the uptick in foreclosures in recent years, there are more people buying up large swaths of properties in East and West Oakland, and then renting them out without fixing health and safety violations. Or the investors purchase them and let them sit empty, she said, waiting for the market to turn around. And because the city can’t prevent such investors from buying at public auctions, or trustee sales, where they pay up-front in cash—reducing the opportunities for low-income families—this proposal is one way to push them to be more responsible, she said.

“We have to look at ways we can control this problem,” Brooks said. “We can control health and safety issues. Those are within our jurisdiction.”

Brooks said this scenario—buyers picking up foreclosed properties with no intention of living there—was not restricted to Oakland. “It’s a phenomenon happening all over the country, where investors are able to come in with cash, and make purchases,” she said. “Then they don’t do anything with the properties, and they sit in disrepair.”

Brooks’ ordinance was stalled last week, when Councilwoman Rebecca Kaplan asked for two amendments to the original proposal, but will be brought back for a vote Tuesday night. Councilwoman Patricia Kernighan, who seconded Kaplan’s alternate motion, told councilmembers that whatever they do adopt should not deter investment.

“One of those things I asked for was to have the ordinance apply only to foreclosed properties or properties that were in the foreclosure process,” Kernighan said. “We’re trying to focus this ordinance on properties that are most likely to be in very bad condition and need fixing up—the ones that are in such bad condition that they’re already causing a problem in a neighborhood.”

-

- Manuel de Paz, an East Oakland resident, said he is attempting to get a modified home loan from Bank of America.

-

- Map, by the Oakland-based Urban Strategies Council, shows that the majority of the properties that have foreclosed upon are in East and West Oakland.

3 Comments

Oakland North welcomes comments from our readers, but we ask users to keep all discussion civil and on-topic. Comments post automatically without review from our staff, but we reserve the right to delete material that is libelous, a personal attack, or spam. We request that commenters consistently use the same login name. Comments from the same user posted under multiple aliases may be deleted. Oakland North assumes no liability for comments posted to the site and no endorsement is implied; commenters are solely responsible for their own content.

Oakland North

Oakland North is an online news service produced by students at the UC Berkeley Graduate School of Journalism and covering Oakland, California. Our goals are to improve local coverage, innovate with digital media, and listen to you–about the issues that concern you and the reporting you’d like to see in your community. Please send news tips to: oaklandnorthstaff@gmail.com.

Sounds to me as though the mortgage holders will be made whole. That is, they will be selling their rights at no loss, whereas if they foreclose, they are likely to lose money.

I’d suggest instead, the city selects a relatively large group of homes, too many for the city to save them all. Ask the mortgage holders to bid on each mortgage a discount they will give the city in exchange for cash. The city then ranks the properties according to the largest discounts. The city then uses it’s money to buy the properties with largest discounts until money is exhausted. City then sells back to current owners as before.

Very good written article. It will be valuable to anyone who utilizes it, as well as myself. Keep doing what you are doing – i will definitely read more posts.

[…] the new program, which was approved by a unanimous council vote and will be funded by a grant from the U.S. […]